How Much Does Baby Alive Cost at Family Dollar

10 Min Read | Jan 24, 2022

Got dependents? Ya need life insurance. Let's talk term vs. whole life.

Life insurance is not a fun topic, but it matters! Your 2 main options are term coverage and whole life. But which is better? The first is a safe plan to protect your family—the second is a rip-off. Nosotros're going to walk y'all through the differences in term vs. whole life now.

What Is Term Life Insurance?

Term life insurance covers you for a specific amount of time. If you get a twenty-year policy, y'all're covered for that 20-twelvemonth term. That'southward why they phone call it "term" insurance. Makes sense, right?

If you lot die at whatsoever point during those xx years, your beneficiaries (the people you picked to inherit your money) receive a payout. For case, if you lot bought a $300,000 policy for a 20-year term and yous die within the next 20 years, your beneficiaries would get $300,000. Yeah, it'southward really that simple.

Compare Term Life Insurance Quotes

And here'southward the key difference between whole life vs. term life: Term life plans are much more than affordable than whole life. This is considering the term life policy has no greenbacks value until you die. In simpler terms, the policy is non worth anything unless the policy owner dies during the course of the term. Term life has ane job: to supercede an income.

Of course, no 1 wants to use their term life insurance policy—just if something does happen, at to the lowest degree you lot know your family unit volition be taken care of. They'll still miss yous, but they won't miss you and wonder how they're going to pay the bills.

What Is Whole Life Insurance?

Whole life insurance (sometimes called cash value insurance) is a blazon of coverage that—you lot guessed it—lasts your whole life. Whole life plans are by and large more expensive than term life. There are a couple of reasons for that, but generally information technology'due south because you're not merely paying for insurance hither.

Whole life insurance costs more because information technology's designed to build cash value, which means it tries to double upwardly as an investment account. Getting insurance and a savings account with one monthly payment? It might sound similar a smart way to kill 2 birds with one stone, only actually, the simply bird getting hit here is your financial future.

What Is the Difference Between Whole Life and Term Life Insurance?

We'll give it to you straight—term life does its job, while whole life tries to practice too many things at in one case. Mixing insurance with investment makes no sense, but that'due south exactly what whole life tries to do. Information technology's like preparation your house true cat to be a watchdog: She might acquire how to scratch a few intruders, but she'll never really guard your belongings, and she'll be a miserable pet.

In the same fashion, a life insurance policy shouldn't be a money-making scheme. It's to provide security, protection and peace of listen for your family unit should the unthinkable happen. Menstruum. Term life is the bulldog of life insurance—you hope you'll never need him to do his thing, but yous're sure equally heck happy to have him effectually the house.

"Life insurance has one job: It replaces your income when yous die." — Dave Ramsey, Complete Guide to Money

Here's another truth about whole life coverage. If you practice the principles we teach, y'all won't need life insurance forever. Ultimately, you'll be self-insured. Why? Because you'll have aught debt, a total emergency fund and a hefty corporeality of money in your investments. Hallelujah!

The lesser line: At that place are far more productive and profitable ways to invest your money than using your life insurance program. What sounds like more than fun to you—investing in growth stock mutual funds so yous tin bask your retirement or "investing" money in a program that's all based on whether or not yous kicking the bucket? We think the reply is pretty piece of cake.

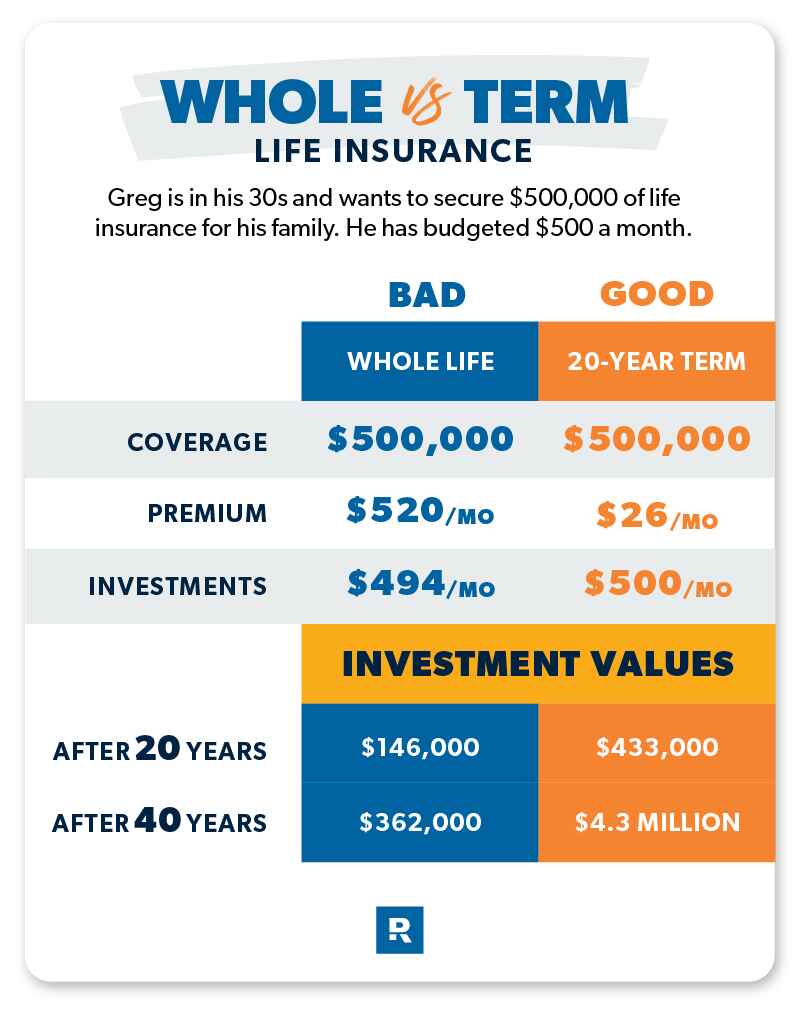

Cost Comparing: Term vs. Whole Life Insurance

Let's say we have a friend named Greg who'due south in his 30s and wants to secure $250,000 of life insurance for his family. He meets with a whole life insurance agent who pitches a $260-per-calendar month policy that will include the insurance coverage plus build upwardly savings for retirement (which is what a cash value policy is supposed to do).

On the other hand, a term life agent tells Greg he tin become a 20-year term with $250,000 of coverage for virtually $13 per calendar month—that's a $247 difference compared to whole life.

If Greg goes with the whole life, cash value choice, he'll pay a hefty monthly premium. But information technology's because the part of his premium that isn't insuring him is going toward his cash value "investment," right? Well, you lot'd call up, merely then come the fees and expenses . . .

In truth, the additional $247 per calendar month disappears into commissions and expenses for the first three years. After that, the cash value portion will offer a horrifically depression rate of return for his investments (nosotros're talking i–3% hither!).

But here's the worst part. Let's say Greg gets this $250,000 whole life policy at 30 years erstwhile. He pays $260 per month, with $15 going to the insurance and the rest into that savings account with a 2% return rate. Afterward 40 years of paying manner also much for his insurance, Greg is 70 and has $250,000 in insurance and roughly $180,000 in cash value. So, Greg dies. How much does the insurance company pay out to his married woman and kids? $250,000. Merely wait, what happened to the $180,000 of Greg's difficult-earned savings? The insurance company keeps it. Sound like a scam? That's considering it is!

You see, but Greg was entitled to the money in that savings account, so he would have needed to withdraw and spend it while he was still alive. Talk near pressure level! Unfortunately, Greg died before he had the run a risk. At present Greg is rolling in his grave equally his insurance agent is staying in a 5-star resort on Greg's dime.

But what if Greg instead chose the $13, 20-year term life policy and decided to invest the $247 per month he'll relieve by not choosing the whole life plan? If he invests in a good growth stock mutual fund with an 11% rate of render, he would have about $214,000 in investments past the fourth dimension his twenty-year term life policy expires and more than $2.1 million at age 70. That's a lot of blindside for your buck! We think Greg volition remainder much easier knowing his family will be staying at that five-star resort.

Term vs. Whole Life Insurance Pros and Cons

Term life . . .

- Is way more affordable.

- Gives y'all the choice to invest however you adopt (instead of locking your cash into a very low-return investment).

- Allows yous to motility toward becoming self-insured.

Simply whole life . . .

- Is far more expensive.

- Tries to do two financial jobs (insurance and investing) at one time but ends up doing neither thing well.

- Delays or stops you lot from always becoming cocky-insured.

- Can pb to having a huge amount of your cash value in the policy disappear if you die without cashing information technology out.

The moral of the story is this: Continue your insurance and your investments dissever. You don't want to spend years investing your hard-earned money only to leave it all to your insurance company. Be smart. Get term life insurance.

Don't Await Until You Need Life Insurance to Get Information technology

Expect, this stuff isn't piece of cake to think almost. But life is precious! Nosotros can't see the time to come and aren't promised tomorrow. The price of non having a plan in place for the unthinkable is much higher than the cost of term life insurance. Y'all need to keep your loved ones protected.

The ideal time to buy life insurance is when you're young and have a make clean neb of health, especially because life insurance companies are all about weighing the risks of the person purchasing the policy. If you're in the marketplace for new life insurance or want an expert to talk to, we recommend RamseyTrusted provider Zander Insurance. Don't let another day go past without being protected. Showtime hither to get your term life insurance quotes.

Term vs. Whole Life Insurance FAQs

How Much Life Insurance Practice I Need?

That'southward easy. You demand policy coverage equal to x to 12 times your annual income. Say you're making $50,000 a yr. You lot need at to the lowest degree $500,000 in coverage. That replaces your bacon for your family if something happens to you. Y'all can run the numbers with our term life reckoner. Quick note: Don't forget to get term life insurance for both spouses, even if i of you stays at home with the kids. Why? 'Crusade if the stay-at-home parent was gone, replacing that childcare and home upkeep would be expensive! If you desire to make certain your family is covered, accept our 5-Minute Coverage Checkup.

How Long Do I Demand Term Life Insurance?

Dave recommends a policy with a term that will run into you through until your kids are heading off to college and living on their ain. That's anywhere from 20 to xxx years depending on your kids' ages. Why then long? Well, a lot of life tin can happen in 20 years.

Permit's say you get term life insurance in your early 30s, when you and your spouse take an adorable 2-year-erstwhile toddler. You lot're laser focused on paying off all your debt (including the house), but you take an heart on retirement planning in the time to come. Fast-forward 20 years—you're both in your 50s and that little pint-sized toddler is now a college grad. The years went past fast.

But look where you are! You're debt-gratuitous—and with your 401(k), savings and mutual funds, you're sitting at a cool internet worth of $500,000 to $one.5 million! By working the program, you were able to build up your net worth and your peace of listen. Now if the unthinkable should happen, even without life insurance, the surviving spouse could alive off your savings and investments. Congratulations, you've become self-insured! Your need for life insurance has shrunk or vanished by at present.

What Happens to Term Life Insurance at the Cease of the Term?

Information technology'south nothing sensational. The policy will simply expire, just you won't find. Y'all'll already be in the coin.

What Information Do I Demand When Getting a Life Insurance Policy?

Applying for life insurance volition mean providing some personal info, then let'south look at a few of the things you'll need to respond as you lot expect for coverage.

- Practise you already have any existing life insurance?

- How's your overall health?

- Any medical history of serious affliction?

- What's your household income?

- How much are your monthly expenses?

- How much debt do yous have, including a mortgage?

- What plans have you made toward retirement?

- What are your plans to encompass college for your children?

- Have you thought almost how you lot want to pay for funeral expenses?

- What'southward your strategy effectually estate planning and tax?

- Do you have a will, and does it include plans for a trust?

- What'south your age?

- The ages of your children?

About the author

Ramsey Solutions

Source: https://www.ramseysolutions.com/insurance/term-life-vs-whole-life-insurance

0 Response to "How Much Does Baby Alive Cost at Family Dollar"

Post a Comment